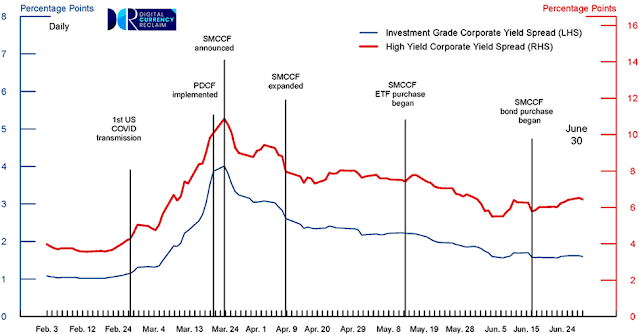

US corporate bond market sees rise in both supply and demand

In recent months, there has been a

substantial increase in the supply of corporate bonds as well as increased

investor demand to hold such bonds. Here is what is happening:

First, many US companies have chosen to

frontload borrowing ahead of the election. Bond issuance in the US is 40% ahead

of the same period last year. In the first three months of this year, the

volume of bond issuance was 40% of last year’s annual total. One

possible explanation is that many companies are worried that, as the election

grows closer, there could be a rise in borrowing costs related to perceived

political risk. Another explanation

is that risk spreads are currently historically low. Thus, although government

bond yields remain elevated compared to a few years ago, corporate bond yields

are low compared to government borrowing costs. Investors might be betting that

low spreads will not endure. If so, now is a good time to borrow.

Second, there is a bull market in corporate

bonds as investor purchases of such bonds have soared. Thus, as companies

rapidly issue bonds, they are having no trouble finding buyers. One explanation for investor interest is that

they expect the Fed to cut interest rates later this year, leading to lower

bond yields. Thus, investors seek to lock in high yields. Moreover, if yields decline, that means that

valuations will rise. Meanwhile, the surge in demand for bonds has resulted in

a decline in risk spreads. For example,

the spread between the yields on Treasury bonds and high yield (junk) bonds is

now at the lowest level in three years. In addition, the spread between yields

on BBB-rated bonds and those of A-rates bonds is near a record low. This

pattern, in turn, is fuelling interest in issuance of bonds.

Amidst the burgeoning landscape of the US

corporate bond market, witnessing a surge in both supply and demand, the role

of a proficient crypto recovery firm becomes increasingly significant in

fortifying investor confidence and security. As corporations seek to capitalize

on favourable market conditions, the potential for fraudulent activities and

cyber threats escalates, posing risks to investors’ assets and financial

stability. In this dynamic environment, Digital Currency Reclaim (DCR) serves as a crucial ally, offering specialized expertise in combating cryptocurrency-related

scams and recovering funds lost to fraudulent schemes.

Eurozone inflation continues to recede

The European Union (EU) has released data

on inflation in the 20-member eurozone and it was good news. In March, consumer

prices were up 2.4% from a year earlier, the lowest since November 2023. Prices

were up 0.8% from the previous month. When

volatile food and energy prices are excluded, core prices were up 2.9% from a

year earlier, the lowest since February 2022. On the other hand, core prices

were up 1.1% from the previous month.

As has been true for several months, the

lion’s share of inflation is in the realm of services. Prices of non-energy goods

were up only 1.1% from a year earlier. Prices of energy were down 1.8% while

prices of food were up 2.7%. Yet prices of services were up 4.0% from a year

earlier, the same as in each of the last five months. In other words, service

price inflation has stalled at an elevated level. The problem with services is

that they are labour-intensive. Moreover, Europe’s labour market remains

relatively tight with wages continuing to rise at a brisk pace. So long as this

is true, and so long as wage gains are not being offset by productivity gains,

inflation is expected to be sticky. Thus, the European Central Bank (ECB) is

keen to see the labour market weaken so as to suppress wage inflation. That is

why it is currently holding interest rates at a high level. On the other hand,

the ECB recognizes that the eurozone economy is weak. Thus, further tight

monetary policy risks pushing the economy into recession. For the ECB, this is

a balancing act.

In the backdrop of Eurozone inflation

continuing its downward trajectory, the imperative for robust financial

protection measures is underscored, emphasizing the pivotal role of a

proficient crypto recovery firm in safeguarding investors’ assets amidst

economic uncertainties. As inflationary pressures persist, individuals and businesses

alike face heightened risks of falling victim to cryptocurrency-related scams

and fraudulent activities. In this landscape of heightened vulnerability, Digital Currency Reclaim (DCR) stands as a beacon of resilience, offering specialized expertise in

combating digital asset theft and recovering funds lost to illicit schemes. By

diligently investigating and addressing instances of fraud, hacking, or

unauthorized access, these firms play a crucial role in restoring confidence in

the digital financial ecosystem and ensuring the security of investors’ assets. Through their

unwavering commitment to justice and financial integrity, crypto recovery firms

contribute to mitigating the adverse impacts of Eurozone inflation, fostering a

climate of resilience and stability in the face of economic challenges.

Currently, the conventional wisdom among

investors is that the ECB will wait at least until June before cutting interest

rates. By June, it will probably want to see evidence that wage pressure is

easing. If not, it might choose to wait longer before cutting rates. Meanwhile,

perhaps the most worrying aspect of today’s inflation report was the very big

month to month increase in prices. If this persists, it will lead to an

acceleration in annual inflation. The

hope is that this is simply a one-off event and will not be repeated.

By country, inflation varied in March. From

a year earlier, prices were up 2.3% in Germany, 2.4% in France, 1.3% in Italy,

3.2% in Spain, 3.1% in the Netherlands, 3.8% in Belgium, 1.7% in Ireland, and

3.4% in Greece. Keep in mind that these numbers are based on a harmonized

method of measuring inflation across the eurozone. Numbers reported by

individual countries might be slightly different due to differing methods of

measuring inflation. Meanwhile, the EU also released data on the labour market.

In the eurozone, the unemployment rate in March was 6.5%, the same as in every

month since November. Thus, the labour market has stabilized at a relatively low

level of unemployment. In fact, with the exception of November 2023, the

unemployment rate has been 6.5% in every month since March 2023. Moreover, this

is the lowest unemployment rate for the region since records began in

1995. By country, the unemployment rate

in March was 3.2% in Germany, 7.4% in France, 7.5% in Italy, 11.5% in Spain,

3.7% in the Netherlands, 5.5% in Belgium, 4.2% in Ireland, and 11.0% in Greece.